Resource Tax Law of the People's Republic of China

Order of the President of the People's Republic of China

No. 33

The Resource Tax Law of the People's Republic of China, adopted at the 12th Meeting of the Standing Committee of the Thirteenth National People's Congress of the People's Republic of China on August 26, 2019, is hereby promulgated and shall come into force as of September 1, 2020.

Xi Jinping

President of the People's Republic of China

August 26, 2019

Resource Tax Law of the People's Republic of China

(Adopted at the 12th Meeting of the Standing Committee of the Thirteenth National People's Congress on August 26, 2019)

Article 1 The entities and individuals that develop taxable resources within the territory of the People's Republic of China and other sea areas under the jurisdiction of the People's Republic of China are the resource taxpayers, and shall pay resource tax in accordance with the provisions of this Law.

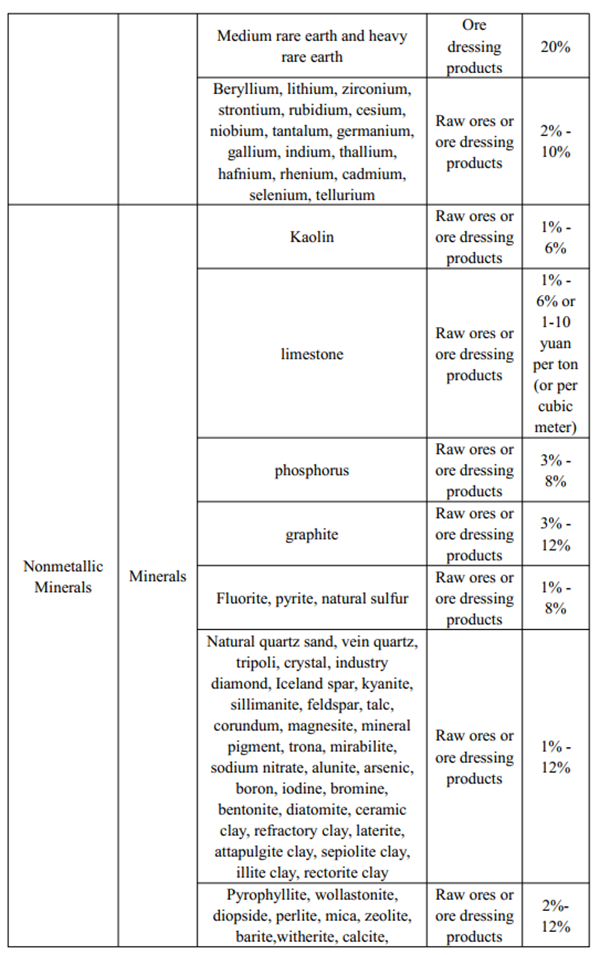

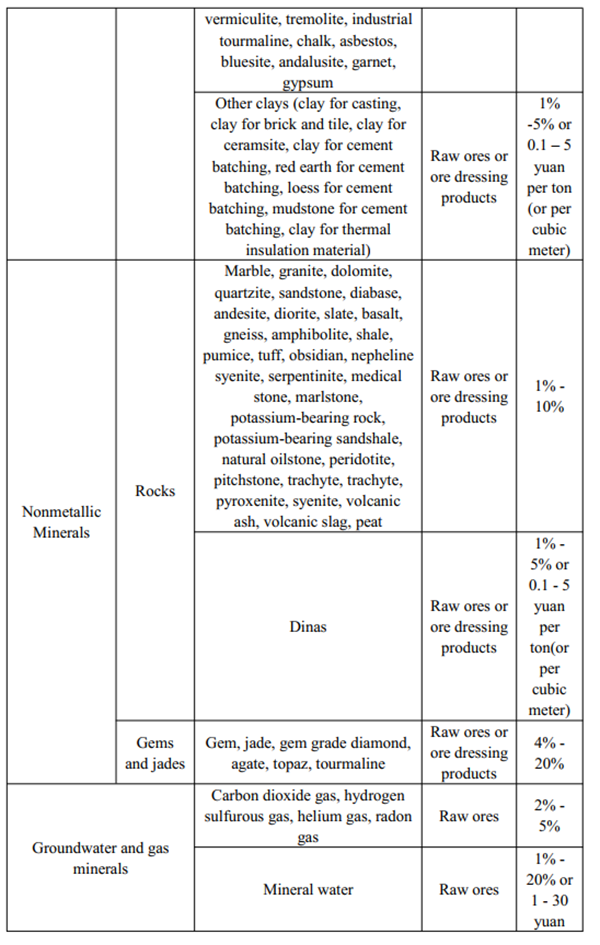

The specific scope of taxable resources shall be determined by the Table of Taxable Items and Tax Rates of Resource Tax (hereinafter referred to as the "Table of Taxable Items and Tax Rates") attached to this Law.

Article 2 The taxable items and tax rates of resource tax shall be governed by the Table of Taxable Items and Tax Rates.

Where a range of tax rates is prescribed in the Table of Taxable Items and Tax Rates, the specific applicable resources tax rates within the prescribed range shall be proposed by the people's governments of provinces, autonomous regions or municipalities directly under the Central Government based on overall consideration to the grade and exploitation conditions of the taxable resources, impacts on the ecology and environment, and other circumstances, and be decided by the standing committees of the people's congresses at the same level, and shall thereafter be filed with the Standing Committee of the National People's Congress and the State Council for the record. Where the taxable items specified in the Table of Taxable Items and Tax Rates are raw ores or ore dressing products, the specific applicable tax rates shall be individually determined.

Article 3 Resource tax shall be calculated and collected as prescribed in the Table of Taxable Items and Tax Rates on an ad valorem basis or on a volume basis.

Where resource taxes may be collected either on an ad valorem basis or on a volume basis, as prescribed in the Table of Taxable Items and Tax Rates, the specific method for calculation and collection shall be proposed by the people's governments of provinces, autonomous regions or municipalities directly under the Central Government and be decided by the standing committees of the people's congresses at the same level, and shall thereafter be filed with the Standing Committee of the National People's Congress and the State Council for the record.

The resource tax payable to be collected on an ad valorem basis shall be calculated by multiplying the amount of taxable resource products (hereinafter referred to as "taxable products") sold by the specific applicable tax rate, and the resource tax payable to be collected on a volume basis shall be calculated by multiplying the sales volume of taxable products by the specific applicable tax rate.

The taxable products that are mineral products shall include raw ores and ore dressing products.

Article 4 Where a taxpayer exploits or produces taxable products under different taxable items, the sales amounts or sales volumes of taxable products under different taxable items shall be calculated separately. If the taxpayer fails to do so or fails to accurately provide the amounts or volumes of taxable products sold under different taxable items, the higher tax rate shall be applied.

Article 5 Where a taxpayer exploits or produces taxable products for the taxpayer's own use, the taxpayer shall pay resource tax in accordance with the provisions of this Law. However, if the taxpayer exploits or produces taxable products for the taxpayer's own continuous production of taxable products, the taxpayer is not required to pay resource tax.

Article 6 No resource tax shall be imposed under either of the following circumstances:

(1) Crude oil and natural gas used for heating in exploiting crude oil or in transporting crude oil within the scope of oil fields; or

(2) Coal gas/coalbed methane (CBM) extracted by a coal mining enterprise for production safety.

Resource tax shall be reduced under any of the following circumstances:

(1) A 20% reduction shall be given to resource tax on crude oil or natural gas exploited from low-abundance oil or gas fields;

(2) A 30% reduction shall be given to resource tax on high-sulfur natural gas, crude oil produced by tertiary oil recovery, crude oil or natural gas exploited from deepwater oil or gas fields;

(3) A 40% reduction shall be given to resource tax on heavy oil or high pour-point oil; or

(4) A 30% reduction shall be given to resource tax on mineral products exploited from mines at the stage of depletion.

The State Council may, according to the needs of national economic and social development, provide exemption or reduction of resource tax under the circumstances conducive to promoting economical and intensive use of resources or protecting environment, among others, and file such tax exemptions or reductions with the Standing Committee of the National People's Congress for the record.

Article 7 Under either of the following circumstances, a province, autonomous region or municipality directly under the Central Government may decide to exempt or reduce resource tax:

(1) Taxpayers suffer heavy losses in the process of exploiting or producing taxable products for reasons such as accidents or natural disasters; or

(2) Taxpayers mine paragenic or associated minerals, low-grade ores, or tailings.

The specific measures for resource tax exemption or reduction as prescribed in the preceding paragraph shall be proposed by the people's government of a province, autonomous region or municipality directly under the Central Government and be decided the standing committee of the people's congress at the same level, and shall thereafter be filed with the Standing Committee of the National People's Congress and the State Council for the record.

Article 8 The amounts or volumes of sales of taxpayers' tax exemption or reduction items shall be calculated separately. If the sales amount or volume is not calculated separately or cannot be provided in an accurate manner, tax reduction or exemption shall not be granted.

Article 9 Resource tax shall be collected and administrated by tax authorities in accordance with this Law and the Law of the People's Republic of China on the Administration of Tax Collection.

Tax authorities, the departments for natural resources and other relevant departments shall establish work coordination mechanisms to strengthen the administration of resource tax collection.

Article 10 Where a taxpayer sells taxable products, the tax obligation arises on the date when the sales payment is received or a voucher for demanding sales payment is obtained. Where the taxable products are for the taxpayer's own use, the tax obligation arises on the date when taxable products are transferred.

Article 11 A taxpayer shall declare and pay resource tax to the tax authority at the place where the taxable products are exploited or produced.

Article 12 Resource tax shall be declared and paid on a monthly or quarterly basis. If tax cannot be calculated and paid based on a fixed period, declaration and payment may be made on a transaction-by-transaction basis.

A taxpayer that makes tax declaration and payment on a monthly or quarterly basis shall, within 15 days from the end of each month or quarter, declare and pay the tax to the tax authority. A taxpayer that makes tax declaration and payment on a transaction-by-transaction basis shall, within 15 days from the date when the tax obligation arises, declare and pay the tax to the tax authority.

Article 13 Any taxpayer, tax authority or any of its staff members that violates the provisions of this Law shall be held legally liable in accordance with the Law of the People's Republic of China on the Administration of Tax Collectionand other applicable laws and regulations.

Article 14 The State Council shall, according to the needs of national economic and social development and under the principles of this Law, collect, on a pilot basis, water resource tax from the entities and individuals that withdraw and consume surface water or groundwater. Whoever is subject to water resource tax shall no longer pay water resource fee.

Differential tax rates are applied based on the status of local water resources, the types of water withdrawn and consumed, local economic development, etc.

The measures for implementing the water resource tax pilot program shall be formulated by the State Council and be filed with the Standing Committee of the National People's Congress for the record.

The State Council shall, within five years from the date when this Law comes into force, report to the Standing Committee of the National People's Congress on the implementation of the water resource tax pilot program, and propose revisions of law in a timely manner.

Article 15 Chinese and foreign enterprises engaging in cooperative exploitation of onshore or offshore petroleum resources shall pay resource tax in accordance with this Law.

An enterprise that has entered into a contract prior to the date of November 1, 2011 on Chinese-foreign cooperative exploitation of onshore or offshore petroleum resources pursuant to law shall, within the period of validity of the contract, continue to pay mineral royalties in accordance with relevant provisions issued by the state, and is not required to pay resource tax; however, it shall pay resource tax in accordance with this Law after the aforementioned contract expires.

Article 16 For the purposes of this Law, the meanings of the following terms are:

(1) "Low-abundance oil and gas fields" include onshore low-abundance oil fields, onshore low-abundance gas fields, offshore low-abundance oil fields, and offshore low-abundance gas fields. "Onshore low-abundance oil field" means an oil field of which the abundance of crude oil reserves per square kilometer is less than 250,000 cubic meters; "onshore low-abundance gas field" means a gas field of which the abundance of natural gas reserves per square kilometer is less than 250 million cubic meters; "offshore low-abundance oil field" means an oil field of which the abundance of crude oil reserves per square kilometer is less than 600,000 cubic meters; and "offshore low-abundance gas field" means a gas field of which the abundance of natural gas reserves per square kilometer is less than 600 million cubic meters.

(2) "High-sulfur natural gas" means the natural gas whose hydrogen sulfide content is more than 30 grams per cubic meter.

(3) "Tertiary oil recovery" means the oil recovery continues by polymer flooding, compound flooding, foam flooding, water alternating gas injection, carbon dioxide flooding, and microbial enhanced oil recovery, among others, after the secondary oil recovery.

(4) "Deepwater oil and gas fields" means the oil and gas fields with a water depth of more than 300 meters.

(5) "Heavy oil" means the crude oil of which the viscosity of formation oil is greater than or equal to 50 mPa per second or the crude oil density is greater than or equal to 0.92 grams per cubic centimeter.

(6) "High pour-point oil" means the crude oil whose pour point is greater than 40 °C.

(7) "Mines at the stage of depletion" means mines with a designed service life of more than 15 years, whose remaining recoverable reserves have dropped to less than 20% of the originally designed recoverable reserves or whose remaining service life is not more than five years. A mine at the stage of depletion shall be determined on the basis of a single mine subordinate to a mining enterprise.

Article 17 This Law shall come into force on September 1, 2020, and the Interim Regulation of the People's Republic of China on Resource Tax issued by the State Council on December 25, 1993 shall be repealed at the same time.

- China's top legislator holds talks with New Zealand House of Representatives speaker

- Chinese, Portugese legislative bodies agree to boost bilateral practical cooperation

- New Zealand House of Representatives speaker to visit China

- Senior Chinese legislator pledges to advance China-Gabon traditional friendship

- Senior Chinese legislator visits Ethiopia