Stamp Tax Law of the People's Republic of China

Order of the President of the People's Republic of China

(No.89)

The Stamp Tax Law of the People's Republic of China, as adopted at the 29th Meeting of the Standing Committee of the Thirteenth National People's Congress of the People's Republic of China on June 10, 2021, is hereby promulgated, and shall come into force on July 1, 2022.

Xi Jinping

President of the People's Republic of China

June 10, 2021

Stamp Tax Law of the People's Republic of China

(Adopted at the 29th Meeting of the Standing Committee of the Thirteenth National People's Congress on June 10, 2021)

Article 1 The entities and individuals that conclude taxable certificates, or conduct securities transactions within the territory of the People's Republic of China shall be taxpayers of stamp tax, and shall pay stamp tax in accordance with the provisions of this Law.

Where entities or individuals, outside the territory of the People's Republic of China, conclude taxable certificates that are used within the territory of China, they shall pay stamp tax in accordance with the provisions of this Law.

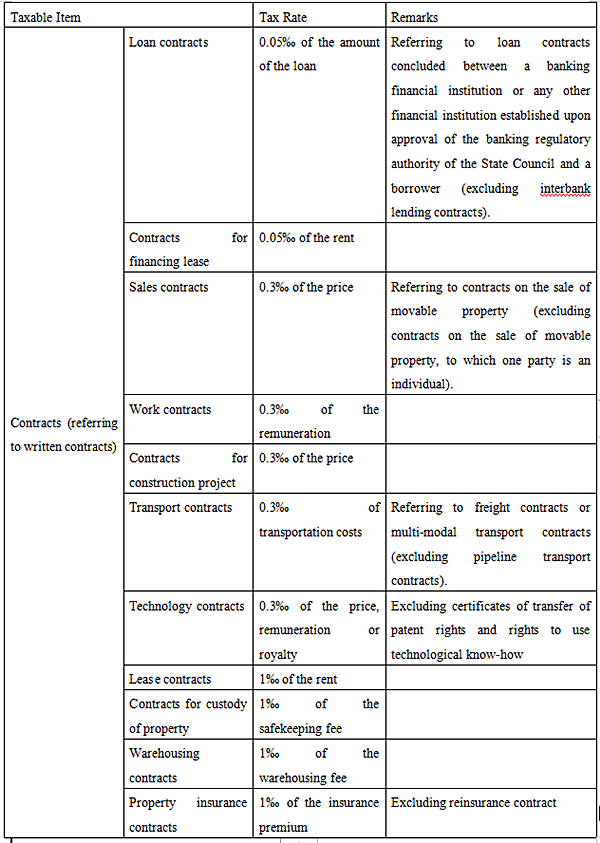

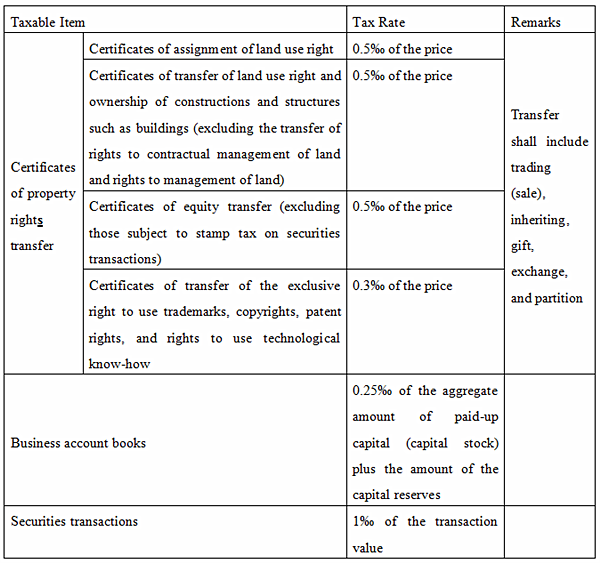

Article 2 For the purpose of this Law, "taxable certificates" refer to the contracts, certificates of property rights transfer, and business account books listed in the Table of Taxable Items and Tax Rates for Stamp Tax as attached to this Law.

Article 3 For the purpose of this Law, "securities transactions" refer to the transfer of stocks and stock-based depositary receipts that are traded on legally established stock exchanges and other nationwide securities trading venues approved by the State Council.

Stamp tax on securities transactions shall be imposed on the transferor instead of the transferee of a securities transaction.

Article 4 The taxable items and tax rates for stamp tax shall be implemented according to the Table of Taxable Items and Tax Rates for Stamp Tax as attached to this Law.

Article 5 The tax basis for stamp tax shall include:

(1) the tax basis for a taxable contract shall be the amount listed in the contract, excluding the amount of value-added tax listed;

(2) the tax basis for a taxable certificate of property rights transfer shall be the amount listed in the certificate of property rights transfer, excluding the amount of value-added tax listed;

(3) the tax basis for a taxable business account book shall be the aggregate amount of the paid-up capital (capital stock) plus the amount of the capital reserves recorded in the business account book;

(4) the tax basis for a securities transaction shall be the transaction value.

Article 6 Where a taxable contract or a certificate of property rights transfer does not list the amount, the tax basis for stamp tax shall be determined according to the amount actually paid.

If the tax basis still cannot be determined according to the provisions of the preceding paragraph, it shall be determined based on the market price at the time of conclusion of the contract or the certificate of property rights transfer; and where government pricing or pricing under governmental guidance shall be implemented pursuant to the law, the tax basis shall be determined according to the relevant regulations of the State.

Article 7 Where there is no transfer price in a securities transaction, the tax basis shall be calculated and determined according to the closing price of the securities on the last trading day before the transfer registration; and where there is no closing price, the tax basis shall be calculated and determined according to the face value of the securities.

Article 8 The amount of stamp tax payable shall be calculated by multiplying the tax basis by the applicable tax rate.

Article 9 Where one and the same taxable certificate specifies two or more taxable items and respectively lists their amounts, the amounts of taxes payable shall be calculated according to their respective applicable tax rates; and where the amounts are not listed separately, the higher tax rate shall apply.

Article 10 Where one and the same taxable certificate is concluded by two or more parties, the amounts of taxes payable shall be calculated separately according to the amounts related to such parties respectively.

Article 11 As to the business account book on which stamp tax has been paid, where the aggregate amount of the paid-up capital (capital stock) plus capital reserves recorded in a subsequent year is greater than the aggregate amount of the paid-up capital (capital stock) plus capital reserves on which stamp tax has been paid, the amount of tax payable shall be calculated according to the increased amount.

Article 12 The following certificates shall be exempt from stamp tax:

(1) duplicates or transcripts of taxable certificates;

(2) taxable certificates concluded by foreign embassies, consulates or representative offices of international organizations in China for the acquirement of premises, which shall be exempt from taxes in accordance with laws;

(3) taxable certificates concluded by the Chinese People's Liberation Army and the Chinese People's Armed Police Force;

(4) sales contracts for the purpose of purchasing agricultural means of production or selling agricultural products and agricultural insurance contracts, which are concluded by farmers, family farms, farmers' professional cooperatives, rural collective economic organizations and villagers' committees;

(5) interest-free loan contracts or loan contracts with discount interest, and the loan contracts concluded by international financial institutions for providing preferential loans to China;

(6) certificates of property rights transfer concluded by property owners for donating property to government, schools, social welfare institutions, and charitable organizations;

(7) sales contracts concluded by non-profit health institutions for the procurement of drugs or medical materials;

(8) electronic orders concluded by individuals and e-commerce operators.

The State Council may, according to the needs of national economic and social development, prescribe stamp tax reduction or exemption in cases such as meeting residents' housing demands, carrying out restructuring and reorganization of enterprises, bankruptcy, and supporting the development of small and micro enterprises, and shall submit such reductions or exemptions to the Standing Committee of the National People's Congress for the record.

Article 13 A taxpayer who is an entity shall file and pay stamp tax with the competent tax authority at the place where it is located; and a taxpayer who is an individual shall file and pay stamp tax with the competent tax authority at the place where the taxable certificate is concluded or he resides.

Where the ownership of a immovable property is transferred, the taxpayer shall file and pay stamp tax with the competent tax authority at the place where the immovable property is located.

Article 14 Where a taxpayer is an overseas entity or individual, if the taxpayer has a domestic authorized agent, the domestic agent shall be the withholding agent; if the taxpayer does not has a domestic authorized agent, the taxpayer shall file and pay stamp tax by itself or himself. The specific measures shall be prescribed by the competent department of taxation under the State Council.

The securities depository and clearing institution shall be the withholding agent of stamp tax on securities transactions and shall file taxes withheld with the competent tax authority at the place where the institution is located and turn over taxes withheld and the interest settled by banks.

Article 15 The time when the obligation to pay stamp tax arises shall be the day when a taxpayer concludes a taxable certificate or completes a securities transaction.

The time when the obligation to withhold stamp tax on a securities transaction arises shall be the day when the securities transaction is completed.

Article 16 Stamp tax shall be calculated and levied on a quarterly, yearly or transaction basis. Where stamp tax is calculated and levied on a quarterly or yearly basis, a taxpayer shall file and pay taxes within 15 days after the end of each quarter or year. Where stamp tax is calculated and levied on a transaction basis, a taxpayer shall file and pay taxes within 15 days from the date when the tax payment obligation arises.

Stamp tax on securities transactions shall be turned over on a weekly basis. The withholding agent of stamp tax on securities transactions shall file taxes withheld and turn over taxes withheld and the interest settled by banks within 5 days after the end of each week.

Article 17 Stamp tax may be paid by pasting revenue stamps or by issuing other tax payment certificates by tax authorities in accordance with the law.

Where revenue stamps are pasted onto taxable certificates, taxpayers shall mark each stamp with a seal on the perforations or draw lines to signify its cancellation.

Revenue stamps shall be printed under the supervision of the competent department of taxation under the State Council.

Article 18 The administration and the collection of stamp tax shall be carried out by tax authorities in accordance with the provisions of this Law and the Law of the People's Republic of China on the Administration of Tax Collection.

Article 19 Where taxpayers, withholding agents and tax authorities and their staff members violate the provisions of this Law, their legal liabilities shall be investigated in accordance with the Law of the People's Republic of China on the Administration of Tax Collection and other relevant provisions of laws and administrative regulations.

Article 20 This Law shall come into force on July 1, 2022, and the Provisional Regulation on Stamp Tax of the People's Republic of China promulgated by the State Council on August 6, 1988 shall be repealed simultaneously.

Appendix: Table of Taxable Items and Tax Rates of Stamp Tax

- China's top legislator holds talks with New Zealand House of Representatives speaker

- Chinese, Portugese legislative bodies agree to boost bilateral practical cooperation

- New Zealand House of Representatives speaker to visit China

- Senior Chinese legislator pledges to advance China-Gabon traditional friendship

- Senior Chinese legislator visits Ethiopia